Philip Barrett and Sophia Chen

What happens to the stock market when social unrest, such as mass protests or riots, occurs? Are investors spooked by this turmoil? Or are we encouraged by the prospect of positive popular change in response to unrest?

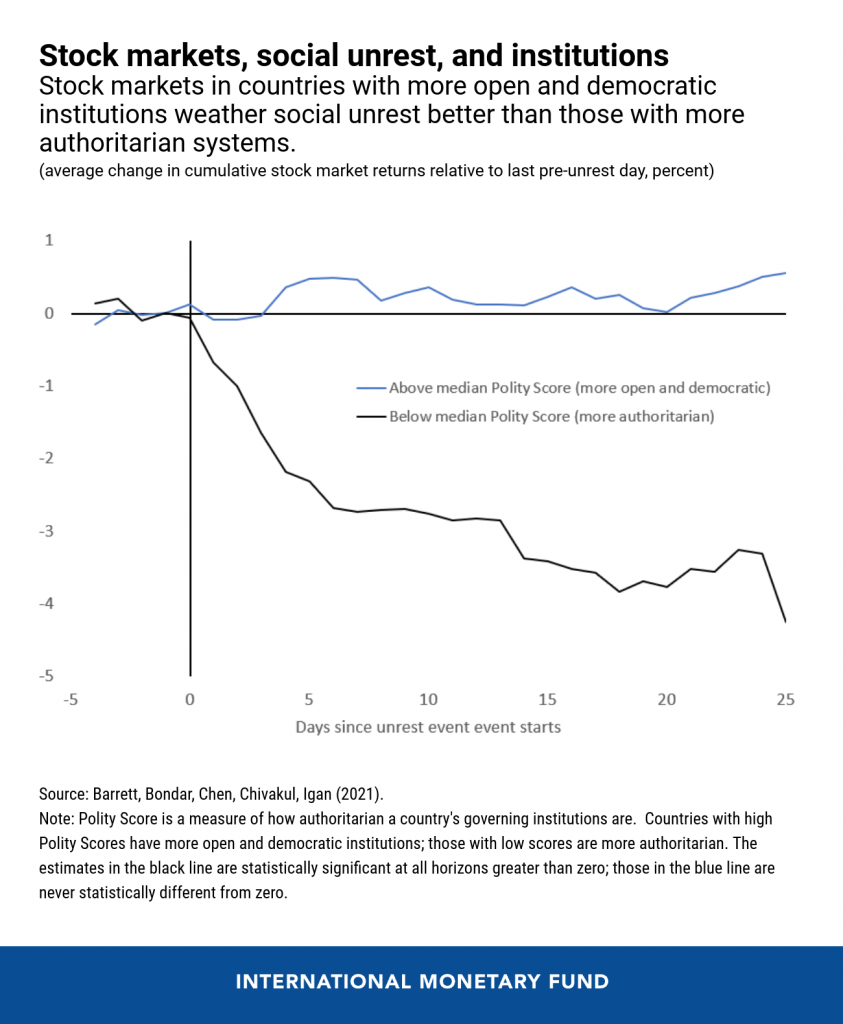

This week’s chart, taken from a recent IMF staff working paper, sheds light on these questions using a new dataset of 156 incidents of civil unrest between 2011 and 2020. Masu. This shows that in countries with more open and democratic institutions, events of social unrest have a negligible impact on stock market returns (blue line). However, in countries with more authoritarian regimes, the impact is largely negative. On average, stock market returns fall by 2% within 3 days and about 4% in the next month (black line).

These findings are consistent with real-world examples. For example, the stock market in France, a country with strong and open institutions, remained largely static in the days after the yellow vest protests began in late 2018.

Of course, differences between countries can arise for a variety of reasons other than political systems. Therefore, we also confirm that this relationship holds even after accounting for other factors that may be correlated with the degree of institutional authoritarianism, such as the severity of insecurity and the country’s income level.

To dig deeper into what kinds of institutions matter, this paper runs further experiments using the six measures of social and political institutions that form the World Bank’s Governance Indicators. Masu. Of these, two factors play an important role in mitigating the stock market’s negative reaction to social unrest events. It is public participation in government and the government’s ability to regulate markets in a way that fosters the development of the private sector.

What investor behavior explains these patterns?

One clue comes from the sharp increase in stock trading volume after a serious disturbance event. Increased trading volume typically reflects increased uncertainty about the outlook, as more trading occurs when investors disagree about the value of an asset. This result suggests that social unrest affects stock market returns through indirect information channels rather than through direct disruptions to economic activity.

Taken together, these results suggest that in countries with high standards of governance, social unrest does not lead to greater dissent or greater uncertainty about future economic performance. This likely reflects the ability of more open institutions to reconcile differing opinions and find compromises.

In contrast, more authoritarian systems may lack this flexibility. There, the ability of financial institutions to adapt to social issues may be reduced, meaning that fear could lead to increased fears of further uncertainty and deter investors.