")

back walker

investment thesis

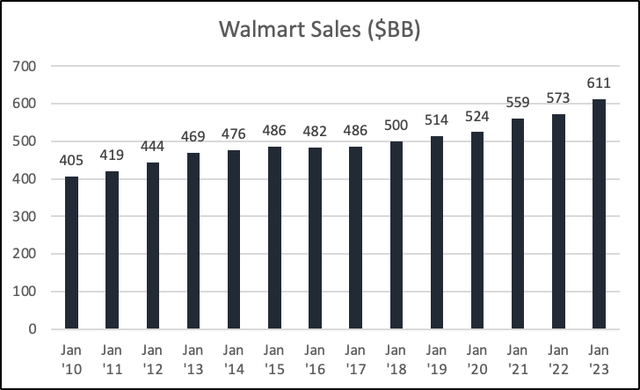

On July 2, 1962, Walmart (New York Stock Exchange:WMT) opened its first store in Rogers, Arkansas. Currently, Walmart is the largest retailer in the United States, with annual sales exceeding $600 billion, and more than 10,000 stores worldwide.i believe Recent post-earnings stock price declines offer long-term investors an opportunity to buy high-quality companies at fair prices. My Buy rating stems from Walmart’s size, stability, strong management team, and attractive valuation.

1. Scale and stability

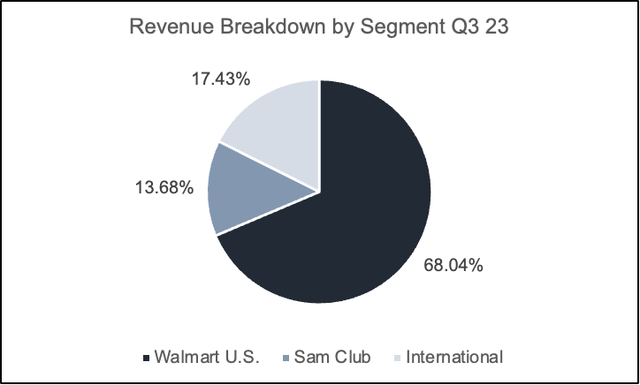

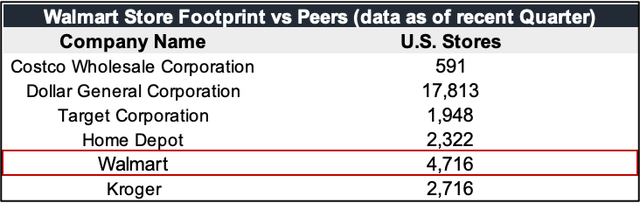

Walmart Inc. is North America’s largest retailer, with a leading retail market share of 47% and a 6.4% market share behind Amazon in e-commerce. Walmart has 4,716 stores in the country, more than double that of rival Target (TGT). In the international sector, WMT has expanded his 5,318 stores.In total, the company The store area is 10,034. Revenue comes from his three segments: Walmart US, Sam Club, and International.

created by the author

Walmart has a simple business model that has worked for decades. It uses its size to buy products at lower prices and resell them at lower prices than its competitors to attract customers. This strategy has made WMT popular among consumers. I don’t believe that a new retail company can exactly replicate the scale of his WMT. That’s not possible. I think the only two companies that could cause problems with WMT are Costco and Amazon. Other than that, we believe WMT will continue to maintain its top market share.

author

As I mentioned in my paper, WMT benefits from recurring revenue and has a high retention rate, so I believe it is a stable business. According to Statista, Walmart has an awareness rate of 93% and a loyalty rate of 60%. The combination of the two and steady returns over the years prove that, as you can see below. Walmart also expects to gain more market share in the near term as consumers tighten up and focus on buying lower-priced groceries.

author

2. Management

You can’t invest in a company without looking at the management team and how they are compensated. The CEO (C. Douglas McMillon) has been with the company for over 30 years. He owns more than 1.7 million shares worth about $270 million. As of 2023, his total compensation was $25.3 million. Of that, he received $19 million in stock compensation. Mr. McMillion has been CEO since 2014. Under his leadership, revenue increased by an average of 2.85% and EPS increased by his 2.68%.

The CFO (John David Rainey) joined the company in May 2022. He has been appointed executive vice president and chief financial officer of Walmart, Inc., effective June 6, 2022. Since he is relatively new to the company, he is not qualified. equivalent shares (167,735 shares). His total compensation as of 2023 was approximately $40 million. Of that amount, $32.6 million was inventory.

My opinion is that management has focused on shareholder returns to date, returning more than $15 billion to shareholders in the form of dividends and stock buybacks in 2023. Given that WMT is now a mature business with few areas left to expand, we do not see this situation changing. Additionally, management has consistently implemented its guidance, only failing to do so in 2023 due to economic headwinds.

author

What causes the pullback?

On November 16, 2023, Walmart reported its third quarter 2024 earnings. The company beat top estimates by $895 million and beat bottom line estimates by $0.01, but the stock ended the trading day down 6.8%. Analysts expect even better, even though WMT raised its full-year sales growth outlook from 4% to 4.5% to 5% to 5.5% and raised its full-year EPS guidance range to $6.40 to $6.48. Was. Management also issued some cautious comments about the outlook for furloughs. The CFO said:

“November sales started to increase as the unseasonable weather eased and holiday events began. So there’s been some dispersion in sales and a reason to be a little more cautious about consumers compared to 90 days ago. did it.”

I believe that a combination of such comments, EPS revisions, and WMT stock trading at all-time highs the day before earnings, caused the ~7% decline. Unless the company notices other trends, I think the fourth quarter results are priced in. That could lead to lower consumer spending in the future.

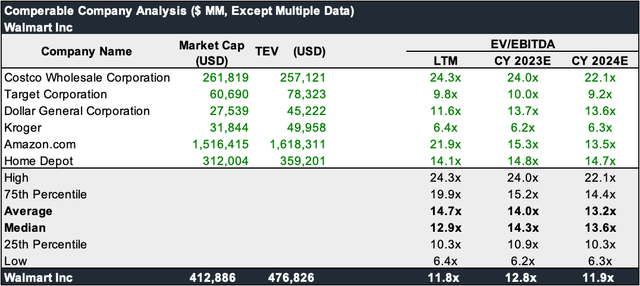

3. Attractive valuation

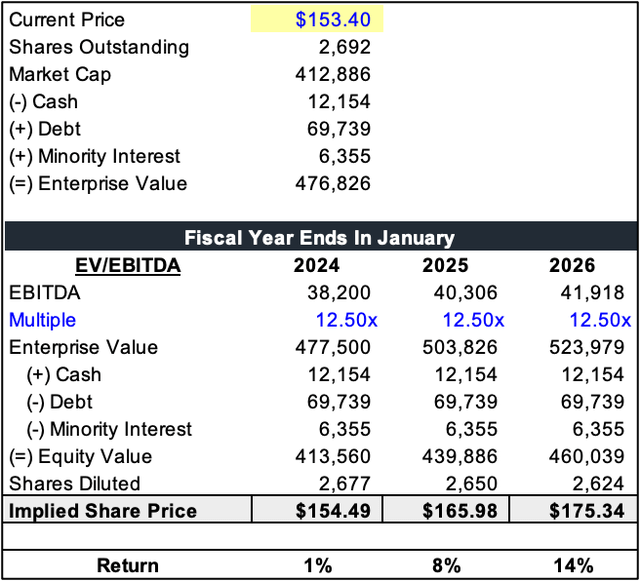

As I write this, the stock price is $153.4. WMT is trading at a forward P/E ratio of 24.05 times the FY23 consensus of $6.47 and 21.92 times the FY2024 consensus of $7.11. On a free cash flow basis, the stock has a yield to enterprise value of over 2.64%. I estimate that revenue will grow at 4.17% annually due to growth in e-commerce, Walmart+, and pricing.

We believe there is significant potential for margin improvement as our advertising, e-commerce and automation efforts advance and begin to bear fruit. Having said that, cost ratio and SG&A margin will be deleveraged by 25 bps and 20 bps in FY24, 20 bps and 10 bps in FY25, and 5 bps in FY26, with EBIT margin of 3.80% and 4.1 %, we expect it to be 4.20%. Each.

author

The multiple used (12.50x) is in line with the company’s FWD multiple, but at a discount versus its competitors. Using the above assumptions, the implied stock price came out to be approximately $166. This translates to a profit of 8.2% at the writing price of this article. Normally, I wouldn’t consider an 8.2% return over 14 months to be a buy, but I think I can make an exception given WMT’s stability, safety, and dominant market position.

author

Main risks

My biggest concern with Walmart is competition. Amazon is already a threat to WMT in terms of e-commerce, but its acquisition of Whole Foods in 2017 has increased competition from brick-and-mortar stores.

Customers prefer shopping at Walmart because they can buy products at low prices. Tighter consumer spending may provide a tailwind, but if inflation rises too much it could increase costs and put pressure on corporate profits.

conclusion

Importantly, WMT’s business model of leveraging its scale to buy products at below-market prices and resell them cheaply has enabled it to become a major retailer in North America. . I like that management is focused on shareholder returns. Despite the company trading 8.2% below my target price, I still assign it a buy due to its stability and defensive nature.