")

scott olson

Walmart (New York Stock Exchange:WMT) will report before the opening bell on Thursday morning, November 16, 2023, with the Street consensus expecting EPS of $1.52, operating income of $6.3 billion and revenue growth of $159.7 billion.

Year-on-year (YoY) growth rates for the three components are expected to be 1%, 5%, and 5%, respectively, so expectations are fairly subdued even though the stock is surging to an all-time high.

For the pivotal January 2024 holiday quarter (WMT’s fiscal fourth quarter), Street consensus currently projects EPS of $1.66, operating profit of $6.8 billion and revenue of $169.4 billion. The year-over-year growth rate is expected to be -3% and +6%. % and +3% respectively.

For fiscal year 2025 (ending January 2025), Walmart “expects” 10% EPS growth on 2% revenue growth, with EPS of $7.11, operating income of $28.7 billion, and revenue of $665 billion. I expect it to be USD. We’ll see how FY25 estimates change over the next few quarters.

Walmart usually provides careful guidance.

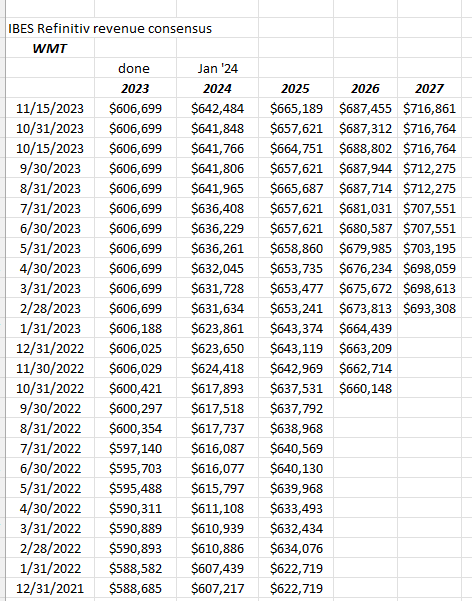

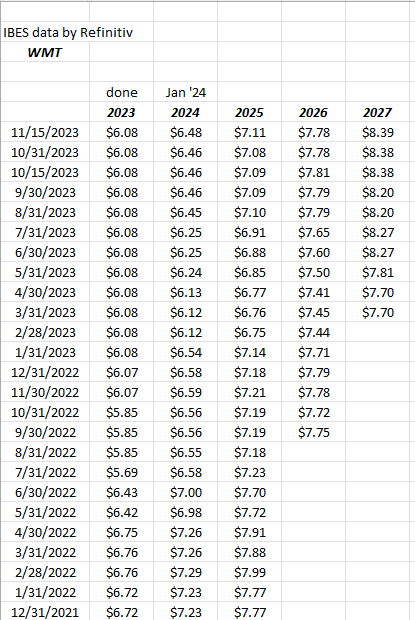

EPS and revenue revisions

Readers should first consider Walmart’s earnings revisions, specifically beyond 2025 (FY25 begins on February 1, 2024), and note the steady increase in earnings estimates.

Next, readers should note the EPS revisions for the same period.

This is a story about the margins. WMT’s steady increase in earnings revisions has led to an uneven trend in EPS revisions. However, this pattern appears to be weakening.

While today’s earnings results for Target (TGT) may get everyone excited about Walmart’s expected earnings report tomorrow, we’d like our readers to know Target’s results for Walmart’s forecast for tomorrow’s earnings report release. I would like to warn you not to apply this.

![]()

Readers should click on the spreadsheet above to see the history of WMT’s inventory-to-sales growth. While WMT started having problems in 2019, probably due to China and the early coronavirus impact, and then work from home solved the problem in 2020, Walmart has I had a serious problem with the chain. And now that too has been fixed.

Target’s October 2022 quarter comparison was also very easy, but Walmart’s October 2022 quarter sales were 3%, but had an unexpected 14% EPS increase. Importantly, there are few easy comparisons for Walmart compared to Target’s October 2022 quarter.

Walmart’s results are positive, but Target’s results are still negative.

At the end of the day, it’s all about margins for Walmart.

Rather than reinventing the wheel, here is a link to WMT earnings preview and post-earnings analysis and summary for August ’23.

I was reminded of Walmart’s July quarterly report earnings preview that the first operating margin decline in 15 years may be due to the fact that groceries account for 50-70% of Walmart’s total revenue. I was wondering if there was. Grocery is a “low margin, high turnover” product that fits very well into the “asset turnover” aspect of his ROE model for DuPont, which itself accounts for a large portion of the margin compression. It may be occupied.

Whatever the cause (and I had attributed much of the margin compression to Amazon’s (AMZN) growing presence), the fact is that grocery margins are low, and groceries make up a large portion of Walmart’s revenue. Margins have declined as the company has grown as a percentage, but with AI and supplier initiatives announced in April 2023, Walmart hopes to further increase its operating margins.

Let’s see how the retail giant’s margins improve in the October 2023 and January 2024 quarters.

Summary/Conclusion: Calendar 2024 results should be cleaner for Walmart (and not just Walmart) as many of the supply chain and logistics challenges are abating, but we will continue to focus on margins and cash flow in the coming quarters. Let’s try this.

An interesting read for blog readers interested in the steel cage battle between Walmart and Amazon iswinner sells all”, a book about Walmart’s evolution into e-commerce by Jason Del Rey.

I enjoy this kind of reading (up to halfway) winner sells all) This is because it provides background and context, and a look at company culture, which is difficult to glean from Wall Street research reports.

Jason looks at the evolution of Walmart’s e-commerce and surrounding areas (Jet.com). In fact, Walmart has been very late to this party, while Amazon hasn’t found an effective solution when it comes to fresh groceries. As long as Walmart’s earnings hold up, its $665 billion in annual sales seems pretty safe, as it’s heavily tilted toward groceries.

In articles I’ve written for www.seekingalpha.com over the past few years, I’ve noted how Amazon’s total revenues are approaching Walmart’s annual revenues (versus WMT’s $665 billion in FY25). Amazon’s 2025 calendar year forecast is $709 billion), but AMZN’s “online store” revenue is only $225 billion of Amazon’s $554 billion in trailing twelve month (TTM) revenue, making it a total Only 50%.

Walmart’s grocery market share is truly a fortress in that it has a “moat,” or susceptibility to disruption. You’d think AMZN would be more into that segment by now, but that’s not the case yet.

I was also thinking about the Kroger (KR) and Albertsons (ACI) merger. One would think that Kroger would be trying to compete with Walmart in the grocery store and maintain the market share it currently has.

Customers own more Walmart stock now than they have in the past decade, but they can’t tell readers that the stock won’t drop $5 to $10 on Thursday morning. There are a lot of moving parts for a retailer of this size, with the stock soaring toward all-time highs.

WMT’s long-term EPS and revenue growth is in the single digits, with revenue likely in the mid-single digits and EPS in the high single digits or low teens.

Supply chain and AI initiatives should help improve margins, but the question is timing.

The stock looks expensive as it trades at 23 times forward EPS (3-year average) and is expected to grow EPS by 5% over the next three years, driven by expected 4% sales growth.

On a sales basis, Walmart’s TTM sales is still an undervalued indicator at 0.62 times, but its cash flow valuations of 11 times and 22 times cash flow and free cash flow appear to be undervalued compared to its PER.

Walmart’s cash flow per share valuation is typically about half of its P/E valuation.

The stock isn’t cheap, but like many consumer staples stocks, it doesn’t look attractive on a valuation basis.

Still, with so much attention focused on large-cap and mega-cap technology, “disruption” and “tech moats,” Sam Walton and Walmart are among America’s original disruptors. With sales of $665 billion and growth expected, Walmart remains one of America’s strongholds.

This is not advice or recommendation. Past performance does not guarantee future results. I could very well be wrong. (All EPS and earnings data comes from Refinitiv’s IBES data.)

thank you for reading.

original post

Editor’s note: The summary bullet points in this article were selected by Seeking Alpha editors.