")

Daniel Aguilar/Getty Images News

investment thesis

Walmart Co., Ltd. (New York Stock Exchange:WMT) will release its quarterly results tomorrow, November 16th, before market. Thanks to strong financial performance over the past few quarters, the company’s stock has performed well since the beginning of the year.Companies rarely ignore consensus Estimate. Therefore, we expect WMT to deliver another strong quarter going forward.

However, there are some red flags from the macro data that indicate management may lower its outlook for the next quarter and the rest of the fiscal year. Moreover, the stock is slightly overvalued according to my valuation analysis. Overall, I will assign a Hold rating to WMT prior to its next earnings release.

Company information

Walmart is not only the world’s largest retailer, but also the world’s largest employer. The company operates more than 10,000 retail stores in 20 countries.

The company’s fiscal year ends on January 31st. Walmart is operated through his three organizations. Segment: United States, Sam’s Club, and International.by Latest 10-K reportIn fiscal 2023, the US segment accounted for 69% of total sales.

finance

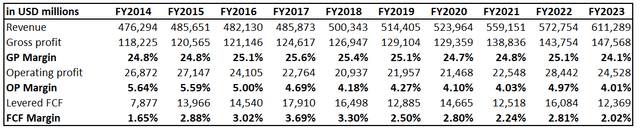

Walmart’s financial performance over the past decade reflects one simple truth. That means traditional brick-and-mortar retail stores are losing out to more convenient e-commerce. Walmart’s revenue has grown at a CAGR of 2.8% over the past decade, which is not much higher than the historical average of US inflation rates. However, in real terms, the company’s profits barely increased. Profitability metrics have also stagnated over the past decade, with free cash flow declining. [FCF] The profit margin in fiscal 2023 was almost halved compared to fiscal 2017, which was the peak of this decade.

Author’s calculations

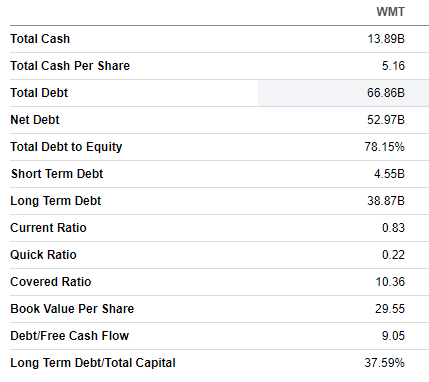

Walmart has a strong balance sheet, with approximately $14 billion in cash as of its latest reporting date. Walmart’s high credit rating and low leverage ratio mean that the company is in a favorable credit position and has strong potential to raise additional debt financing if needed. Despite its razor-thin profitability metrics and capital-intensive business model, Walmart’s consistent dividend increases and aggressive share buybacks demonstrate a commitment to shareholder value and a sound capital allocation approach.

In search of alpha

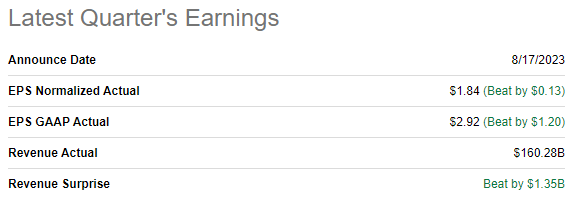

The company’s latest second-quarter results were released on August 17th, and the company beat consensus estimates. Revenue increased 5.9% year over year, and adjusted EPS expanded from $1.77 to $1.84. We would like to emphasize that operating leverage did not contribute much to year-over-year EPS growth, as operating margin only expanded by 5 basis points.

In search of alpha

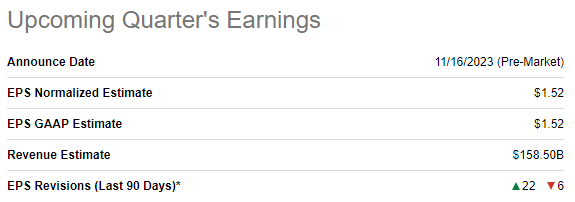

We won’t delve further into the details of the latest quarterly results, as the company will announce its fiscal third quarter 2024 results before market tomorrow. So you better prepare for the upcoming earnings release. Consensus estimates call for quarterly revenue of $158.5 billion, representing year-over-year growth of 4.6%. Adjusted EPS is expected to be roughly flat by consensus. Walmart rarely misses consensus estimates for revenue and his EPS. Therefore, third-quarter profits are also likely to be better than expected.

In search of alpha

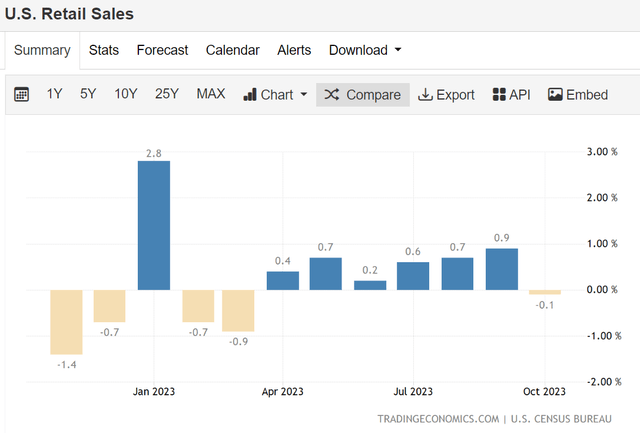

While the consensus expected movement in WMT’s financial performance looks solid, we think guidance will be important for investors. The latest U.S. retail sales data suggests a softening macro environment that Walmart will need to navigate in the fourth quarter. According to the latest report, US retail sales recorded a slight decline of 0.1% in October. Even a small decline like this could signal a potential change in consumer spending patterns, which could lead to a reduction in the company’s fourth-quarter operating plan. Seems like a potential red flag to me.

tradingeoconmics.com

US consumer confidence index [CCI] The third consecutive month of decline in sales in October also does not create optimism for WMT’s upcoming earnings release. In my opinion, this downward trend in consumer confidence complicates an already difficult macroeconomic situation. Despite its low-price business model, Walmart is likely to face headwinds if consumers become more cautious and conservative in their spending patterns.

With the Fed’s monetary policy tightening and Jerome Powell still sending hawkish signals, I don’t expect consumer confidence to recover quickly. Even though inflation subsided in October, there are still some big reasons why the fight against inflation is far from over. First, oil prices remain high despite the recent pullback from strong storage data. Second, geopolitical tensions are rising around the world, with two major military conflicts currently taking place in Ukraine and Palestine. A “cold war” continues between the world’s two largest economies, the United States and China. Geopolitical tensions will lead to deglobalization, and the most cost-effective supply chain routes will be severely disrupted, driving up inflation. That said, Walmart management is likely to emphasize a cautious outlook on the company’s near-term outlook.

Overall, we expect Walmart’s earnings report to be mixed. The company is likely to deliver strong results in the third quarter, beating consensus estimates, but given the fact that the U.S. economy is cooling, it is also likely that its outlook for the rest of the fiscal year will be revised downward.

evaluation

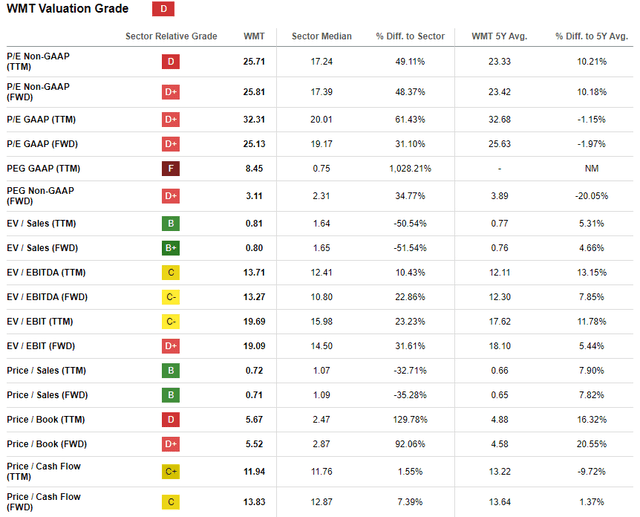

The stock has risen 17.5% since the beginning of the year, slightly underperforming the broader U.S. market. The current valuation ratio is not far off from the company’s historical average, which means the stock is approximately fairly valued. WMT’s brand strength and scale of business are unparalleled, so we’ll ignore comparisons between multiples and sector medians.

In search of alpha

Despite WMT being a dividend machine with 49 consecutive years of increasing dividends, we do not intend to simulate a dividend discount model. [DDM] here. Given its very low forward dividend yield of 1.36% and the modest pace of dividend growth over the past decade, this stock is clearly overvalued from a DDM perspective.

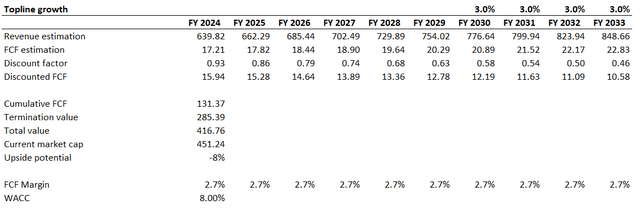

That being said, I prefer to proceed with discounted cash flows. [DCF] approach. I use the 8% WACC suggested by Gurufocus. I set his FCF margin at a flat rate of 2.7%, which has averaged over the past 10 years. Consensus revenue estimates are available through FY2029, with an expected CAGR of 3% thereafter.

Author’s calculations

According to my DCF simulation, Walmart Inc.’s fair value is approximately $417 billion, 8% below its current market cap. We think the 8% premium for WMT stock is reasonable given the company’s strong brand and massive scale. Walmart’s current stock price of about $170 seems reasonable to me.

conclusion

In conclusion, WMT is on hold before the third quarter results. Stellar’s surprising performance suggests the company will likely beat consensus revenue and EPS estimates, which is a good thing. But still, investors may be disappointed after the earnings release, as there are several big reasons why a guidance cut is very likely to occur. Last but not least, Walmart’s valuation is also not attractive.